Log In

To sign in to the NCB Dispute Portal, enter your NCB Online username and password in the field below:

TERMS AND CONDITIONS

THIS AGREEMENT EXPLAINS THE TERMS OF OUR CREDIT CARD PLAN AND GOVERNS ITS USE AT ALL TIMES. PLEASE READ IT CAREFULLY.

In this Agreement, the words “you” and “your” refer to each and all of the persons who use a credit card issued by us or under an account we hold. The words “we”, “us” and “our” mean National Commercial Bank Jamaica Limited and its successors and assignees.

Card means the credit card currently issued to you.

Balance is the total amount of all transactions, fees, interest, bank charges and other amounts payable under this Agreement which have been posted to your account, less any payments or other credits which have been posted to your account.

Cardholder means the Primary Cardholder and any Authorized User.

Insurance Company means NCB Insurance Company Limited.

Credit Card Insurance (CCI) means protection against outstanding Credit Card obligations in the event the Primary Cardholder dies (Life Only) or is diagnose with a specified Critical Illness (Life & Critical Illness) leaving an outstanding card balance(s).

Primary Cardholder means the person who applied for a Card, whose name is on the account and to whom a Card has been issued.

Authorized User or Additional Cardholder or Co-Applicant means the person to whom a Card has been issued as authorized by the Primary Cardholder.

Balance Transfer means a charge to your Card to pay off the outstanding balance on another credit card account.

Cash Advance includes Cash-Like Transactions, and a charge to your Card to get cash taken at an ABM or at our Branches or at another Bank or financial institution.

Cash-Like Transaction means a transaction involving the purchase of items directly convertible into cash and are similar to cash including casino gaming chips, money orders, wire transfers, travellers’ cheques and gaming transactions (including betting, off-track betting, and race track wagers and casino gaming).

When the cardholder accepts, activates, signs or use the card, it means that you agree to the terms in this agreement.

Security

You must do all that you reasonably can to keep the Card safe and the Personal Identification Number (PIN) secret at all times. You must never allow anyone else to use your Card. You must sign the Card before you can use it.

Card Use

You may use the Card to purchase, rent or lease goods or services from persons who honour the card. Purchases or Cash advance done in a foreign currency on a card that is billed in Jamaican dollars will be converted at the days rate as determined by us and may include conversion and other costs associated with the transaction at the date it is posted to the account. Credits from merchants are subject to daily rates and may be converted at a different rate from the original transaction. You may obtain loans (cash advances) from any licensed financial institution and ABM that accepts the card. You may also use the card to pay taxes, duties or government charges. Whenever you use your card, you shall sign a sale or cash advance voucher. If this is not done (for example where the transaction is by mail order by telephone, internet, or facsimile) you will still be liable to pay us all the amounts charged to your card account. This Card and account (and supplemental cards which are used by Authorised Users) is for your use only and should not be used by others. You agree not to use the card for anything that is illegal or fraudulent. The use of this Card will always be subject to any statutory restrictions or regulations imposed by the Bank of Jamaica.

Credit Limit and Overlimit Fee

Your credit limit will be advised when we send you your Card(s) and on each monthly statement. We may periodically change your card limit, and we will notify you if we do. The Balance at any time must not be more than your credit limit. Where the Balance is in excess of your credit limit an Overlimit Fee will be applied. For the avoidance of doubt, please note that where any charge or fee is made against the account as provided for in this agreement, irrespective of whether you are aware of same, an Overlimit Fee will be applied If you request credit in any form which if granted, would result in your total outstanding balance, including authorized purchases and payments of government or other charges not yet posted to your account, being more than your credit limit (whether or not the balance before the request for credit was more than the credit limit), we may: Grant the request without permanently raising your credit limit, Grant the request and treat the amount which is more than your credit limit as immediately due, or Refuse to grant the request. We may advise the person who made the request that it has been refused. If we have previously granted requests for credit over your credit limit, it does not mean that we will grant any further overlimit request. Amounts in excess of approved limits will attract an additional charge for both local and international accounts. Only one Overlimit fee will be charged per statement period. All Cardholders are jointly and severally liable for the liabilities outstanding on the account.

Payment

You promise to repay us the total Balance on your account. You may pay the entire Balance outstanding at any time before the payment due date. Payments are applied towards interest first and then to fees, Balance transfers, Cash Advance, adjustments, and then to purchases. We reserve the right to refund amounts which overpay your account. Each month you must pay at least the minimum payment due shown on your monthly statement. The minimum payment each month will be a percentage of your current balance plus any past due amount and shall be paid by the payment due date. If your account is in excess of the Credit Limit you are required to pay the excess portion in full, plus at least the minimum payment. Where we offer the option of not making a minimum payment (payment holiday) interest will continue to accrue. If payment is made by cheque, we reserve the right to hold the funds against the account until the cheque is cleared. If your payment cheque is returned unpaid for any reason; we will charge your account a Returned Cheque Fee for each returned cheque. In the event of your non-compliance with our request for full repayment of all outstanding balances on your credit card account, we may use the services of a debt collector and /or Attorney-at-Law to obtain repayment. The resultant cost for such services will be payable by you and will become part of the debt owed by you.

Insurance premiums:

Where applicable, premiums will be calculated based on the outstanding balance of the previous month’s Credit Card Statement up to a maximum of JA$2,500,000.00. The premium is calculated at a rate per $100 and will be charged to the Credit Card account monthly.

Our rights if you default:

If you do not make the required payment by the payment due date, fail to abide by any of the terms of this Agreement, become bankrupt or insolvent, make any false or misleading statements on your application for this account, default on the payment of any other obligation to us, your property is seized by garnishment, attachment or any other process by any creditor, legal action against you is pending or in progress that will prohibit the Bank lending to you (in which case all other accounts will also be frozen). We may terminate your account and we may take the

following actions:-

1. Demand full immediate payment - The entire Balance owing on the account will, at our option become due and payable with interest at the annual interest rate payable on the account at the time;

2. Fix the minimum payment at the existing or a new percentage of your outstanding balance at the time of default or a specified dollar amount, even if greater than the amount previously in effect; Your future minimum payments will then be fixed at that amount until your account has been paid in full;

3. We may without notice to you recover outstanding monies by deducting money from any other account that you have with us or any of our NCB Group entities and applying those sums to your account; and/or

4. Request that you cut the Card(s) and return them to us.

In the event of your death receivership or insolvency

We shall require immediate payment from your estate/receiver/liquidator ( as applicable) of all amounts due and owing. (Cardholder covered under CCI) - If the Primary Cardholder dies under either option or is diagnosed with a specified Critical Illness (if covered under Life & Critical Illness option), we shall apply to the Insurance Company for settlement of the outstanding Credit Card balance up to a maximum of $2,500,000.00. (Cardholder is not covered under CCI), we shall immediately freeze your account and shall require immediate payment from your estate of all amounts due and owing. Where the Primary Cardholder dies then the other Cardholder(s) shall remain liable for all outstanding amounts on the account(s). Our failure to exercise any of our rights when you default does not mean that we are unable to use those rights at a later date.

Refusal to honour your card

We are not liable for any refusal to honour the Card or for any retention of a Card by us or by any seller of goods or services or by any government department or agency nor are we liable for any loss. In the event that we incur any liability to you or anyone claiming through you, such liability if not excluded hereunder shall in all circumstances be limited to $100.00.

Termination

We may end this Agreement or withdraw or limit your right to access the account at any time without telling you in advance for any reason (including the reasons set out in the MATERIAL ADVERSE CONDITION CLAUSE ). You may terminate this Agreement at any time by notifying us that you are cancelling your account by repaying same in full or in such manner as we may agree and by returning all Cards issued on the account. Whether we end the Agreement or you end the Agreement it will not affect your obligation to pay all amounts owing on the Account.

Interest and Grace Period

We will not charge you Interest on purchases and other fees if you pay the statement balance on or before the payment due date on your statement. The interest-free period is not applicable to Cash Advances and Balance Transfers. Interest on Cash Advances and Balance Transfers are accrued and charged, from the transaction date until repaid in full, and is shown on your statement as “interest on cash advance”. The number of days between the statement date and the payment due date on your statement is the Grace Period. If we do not receive payment in full by the payment due date, daily interest is accrued on all debit type transactions posted to your account from the transaction date. Interest accrued on purchases and other charges in the previous billing cycle will be charged to your account. We will charge this interest at the relevant rate using the average daily balance. This is calculated as the cumulative balance on the account divided by the number of days for which interest is being charged. We may change this rate at any time and from time to time in our absolute discretion. Interest charges on local and international credit cards are calculated as a percentage** per annum.

Monthly Statements

We will normally provide a monthly statement (which statement can be provided electronically) showing your payments and all amounts we have charged to your account since the last statement. A printed statement will be made available on request. It is the responsibility of the cardholder to call our Customer Care Centre or visit our website to obtain payment, interest or due date information. Interest will not be waived in the event of non-receipt of your statement.

Limiting your right to use the card

In our absolute discretion, we may refuse to approve a transaction, cancel or suspend your right or an Authorized User’s right to use any Card issued by us for any or all purposes or refuse to replace any Card without first telling you. This agreement will continue even if we act upon any of the above mentioned criteria. We will not be liable if we do not approve a transaction, if you or your Authorized User cannot use the Card for a transaction or for any loss or damage you or any Authorized User suffer as a result of the way you are told this.

Account fees

All fees, duties or charges arising in connection with the Card and/or the Cardholder Agreement and/or the collection of monies due in relation to the Card are for your account. An annual membership fee** is charged on every account for both the Primary and supplemental card(s) whether or not the account is used. The fee will be charged on joining and on each anniversary date of the opening of your account. If you decide to cancel your account, you must notify us within 30 days from the closing date of the fi rst billing statement which refl ected the fee in order for us to refund this fee and cancel your account. Otherwise, the fee is not refundable. Membership fees vary according to card type and current rates may be obtained from us. If any of the cards on your account are lost, a fee** will be charged if we provide you with a new account and new cards. We will charge your local and international accounts a late payment fee** if your minimum payment is not received by the due date. You will also be charged an overlimit fee if you exceed your authorized limit**. If you ask for copies of itemized transactions refl ected on statements or copies of statements which prove to have been made by you, a charge will be levied**.

Special Offers

The extension of special offers to you will override this agreement or any other terms and conditions applicable to this card from time to time, only to the extent that the offer is inconsistent with this agreement and/ or terms and conditions, while the special offer is in progress.

Reward

Card rewards are generated on net purchases, that is, purchases minus reversals. Payments of your accumulated rewards are subject to

conditions as follows;

1. Account is not delinquent at the time reward is to be paid.

2. Account is still opened.

3. An annual total cap, which may be modified by notice sent prior to the start of the year in which the rewards are earned.

4. Any other terms and conditions applicable to the card from time to time.

Indemnity

1. By providing an email address, facsimile number and telephone/mobile number, you authorize the Bank to contact you by these means. This includes sending your confidential information to you at your request;

2. That the Bank may act on any electronic mail or facsimile instructions given by you from time to time and you voluntarily and with full knowledge take and assume any and all risks associated therewith;

3. Once the electronic mail or facsimile instructions have been sent to the Bank purportedly by the person (or by any of the persons, if more than one) authorized from time to time to sign in accordance with the mandate or other valid instructions from you to the Bank, the Bank shall have no obligation to check or verify the authenticity or accuracy of such electronic mail or facsimile instructions purporting to or have been sent by you (regardless of whether the Bank may have, or may in the future, choose to so check or verify) and may act thereon as if same had been duly given by you;

4. That in acting on electronic mail or facsimile instructions the Bank shall be deemed to have acted properly and to have fully performed all obligations owed to you, notwithstanding that such electronic mail or facsimile instructions may have been initiated, sent or otherwise communicated in error or fraudulently and you shall be bound by such electronic mail or facsimile instructions if the Bank has in good faith acted in the belief that such electronic mail or facsimile instructions were given by you;

5. You shall not provide the Bank with written instructions bearing original signature(s) where prior instructions to effect the same transaction have been sent to the Bank by electronic mail or facsimile. You acknowledge that where electronic mail or facsimile instructions are followed by subsequent written instructions bearing original signature(s) contrary to the above, this may lead to the Bank giving effect to these instructions more than once. You acknowledge that in such event you shall bear the risk of such duplication occurring and shall indemnify and hold the Bank harmless against all losses,liabilities, claims or damages which may arise as a result of the Bank acting more than once on such duplicated instructions;

6. That the Bank may, in its absolute discretion, decline to act on or in accordance with the whole or any part of electronic mail or facsimile instructions pending further enquiry to or further communication by you, so however that the Bank shall not be under any obligation to so decline in any case and the Bank shall in no event or circumstances be liable in any respect for not so declining; and

7. To release the Bank from and indemnify the Bank against all claims, losses, damages, costs and expenses howsoever arising in consequence of, or in any way related to, the Bank having acted in accordance with the whole or any part of any electronic mail or facsimile instructions or having exercised (or failed to exercise) the discretion conferred upon the Bank in clause 5 above.

Communicating with you

Communication to the Primary Cardholder will be sufficient communication to all Cardholders. Communication sent by mail will be considered to have been received by the Cardholder seven (7) business days after we mail it or at the time of sending in the case of an electronic method of contact or when received if delivered by hand. The Primary Cardholder must give us prompt written notice of any change to your account information including a change to your address information, telephone numbers or e-mail address. We are not responsible for the failure of the Primary Cardholder or any Authorized User to receive a statement or other communication.

General

We can delay enforcing any of our rights under this Agreement without affecting any of our rights hereunder. We may investigate your credit history, employment and income and may verify your credit references. We may disclose information about your account including the way you pay this account to credit reporting agencies, to our subsidiaries and affiliates, to debt collectors, to any other party at our sole discretion, and when required by legal process. There is a charge for credit reports provided to other financial institutions at your request. This charge will be debited to your account on mailing of the report and will be reflected on your monthly statement with an appropriate notation. We shall not be liable if we are unable to perform our obligations due directly or indirectly to the failure of any machine, data processing system, or transmission link or due to industrial dispute or to any cause outside of our control or the control of our agents, servants or sub-contractors. If any part of this Agreement is found to be invalid, the rest remains effective. All Cardholders are individually and collectively responsible for any Balance for any unexpired Cards until they are returned to us. From time to time, we may require you to provide us with up to date credit information. The card is our property and may be recovered by us at any time; you must return it to us on request. The Cardholder shall immediately notify National Commercial Bank Jamaica Limited in writing of any change of name or address. Credit Card Insurance does not cover balances in the event of default. You shall not use your Card to pay any installment on an existing debt. Requests for banker’s reports and other documentary items will be honoured at a fee**. All fees and rates are subject to change from time to time without notice.** Current fees/rates are available at all NCB Branches and via the internet at www.jncb.com.

Your Billing Rights

If you think your bill is wrong, or if you need more information about a transaction on your bill, write to NCB, P .O. Box 445, Kingston 10. We must hear from you no later than 25 days after we have sent you the first bill on which the error or problem appears. You may telephone us, but doing so will not preserve your rights. In your letter, please state:Your name and card number The dollar amount of the suspected error The error and why you believe there is an error. If you need more information describe the item you are not sure about. If you have authorized us to pay your credit card bill automatically from your savings or checking account, you can stop the payment on any amount you think is wrong. To stop the payment, your letter must reach us three business days before the automatic payment is scheduled to occur. If the card is lost or stolen the Cardholder must immediately notify NCB, 10 Oxford Road, Kingston 5. If notification is given orally, it must be confirmed in writing within 7 days. Until we receive written notification, the Cardholder will be liable in respect of any sale or cash advance vouchers issued against the lost or stolen card. The Cardholder’s liability for subsequent sale, cash advance and/or payment of government charges (other than those made by the Cardholder) will cease on the day following the receipt by us of such written notice of any loss or theft of the card. The Cardholder will give us all the information in his or her possession as to the circumstances of the loss and take all reasonable steps to assist us to recover the missing card.

Material Adverse Condition Clause

We may end this Agreement or withdraw or limit your right to access the Account where there is evidence of a Material Adverse Condition. A Material Adverse Condition is evidenced by one or more of the following conditions::-

a) Signifi cant additional borrowings from other sources/financial institutions

b) Non- compliance with terms and conditions of the Agreement

c) Material reduction in security margins or values

d) Reduction in or development of factors that are likely to reduce your cash fl ows, profi ts or tangible net worth

e) Reduction in credit balances below required minimum levels

f) Indications of weakness in internal controls

Lost/Stolen Cards

For emergency assistance or to report a lost/stolen card, please call:

1-888-429-5477 : Jamaica

1-888-429-5477 : USA and Canada

1-888-429-5477 : Collect

Changing Terms of this Agreement

This Agreement is made in Jamaica and is governed by the Laws of Jamaica. We may change the terms and where notice is required by law, we will inform the Primary Cardholder in writing at least 30 days before the effective date of the change. The change will apply to all unpaid balances in your account or if you sign, use or activate any Card or the Account. Benefits, services and coverages associated with any Card or the Account may also change or end by giving subsequent notice to you, unless advance notice or notice in some other way is required by law. You can avoid the new terms if you return all cards, pay the unpaid balance in full and make no further charges to your account. You must do these things before the new terms go into effect.

Ending this Agreement:

We may end this Agreement or withdraw or limit your right to access the Account at any time without telling you in advance. You may also end this Agreement by giving us notice in writing. Whether we end the Agreement or you end the Agreement it will not affect your obligation to pay all amounts owing on the Account.

FAQs

-

-

Who are cardholders and merchants?

- A cardholder is a customer that owns the credit card used to facilitate credit card transactions.

- A merchant is the provider of goods and services that accepts credit cards as a means of payment.

-

What is a representment?

- This occurs when the acquirer (Merchant) refutes or returns the Dispute request by providing documentation to substantiate the charge.

-

What is Pre-Arbitration / Second Presentment?

- A Pre Arbitration or Second Presentment is the final chance an Acquirer (Merchant) has to resolve a dispute with the Issuer (Card Holder) before it is escalated to Visa or MasterCard for them to make a FINAL ruling on the case.

-

What is Arbitration?

- An Arbitration is the final stage of the Dispute process. If the Issuer (Cardholder) is unable to resolve the dispute with the acquirer (Merchant) then a case is filed with Visa/MasterCard to decide which party is responsible or liable for the disputed transaction(s). This decision is final and must be accepted by both parties.

-

What is a Provisional Credit?

- A provisional credit is the interim reversal of a transaction, pending the outcome of an investigation. The transaction can be re-applied based on the finding of the investigation.

-

How Long After a Transaction can I raise a dispute?

-

The Dispute request should be raised within

100 days of the transaction. -

The Provisional Credit will be applied to the customer’s account and held for

10 days days pending the outcome of our investigations. -

Generally, the Provisional Credit will be released after

10 days. However, the hold can be extended based on the outcome of our investigations.

-

The Dispute request should be raised within

-

Can I Update my contact information?

- Yes, you may update your contact information my using the Update Contact Information feature to change your cell phone number, email address or mailing address using RSA verification.

-

Fees?

These Fees are ONLY applied if it is found that the Card holder is at fault.

-

Research fee on non-Jamaican Currency transactions

– US$25.00 . -

Research fee on Jamaican Currency transactions

– JA$ 850.00 . -

US$500 arbitration/compliance fees

-

Research fee on non-Jamaican Currency transactions

-

How do I report my card as lost, stolen, not received or damaged?

-

To report your card lost, stolen, not received or damaged click on the "Request a Replacement Card” tab and complete the form.

If you still need to speak to a customer care representative

Click Here for a list of all emergency contact numbers.

-

To report your card lost, stolen, not received or damaged click on the "Request a Replacement Card” tab and complete the form.

If you still need to speak to a customer care representative

-

Are there any fees associated with reporting lost, stolen card, not received or damaged?

- Stolen or damaged cards do not attract replacement fees. However, fees associated with replacement of lost card are product specific and in accordance with existing schedule of rates and charges.

-

How long after reporting my card lost, stolen, not received or damaged will I get a replacement?

- Cards reported lost, stolen, not received or damaged are immediately replaced and dispatched for collection within three (3) working days from the post office.

-

Can I cancel the report, If my card is found after reporting it lost or stolen?

- Cards reported lost, stolen, not received or damaged are immediately replaced and subsequently dispatched for collection. Therefore, due care must be taken prior to making report as this cannot be cancelled after submission if card is found

-

How do I block/unblock/ my card?

-

Select block or unblock a card tab and click the button

on the appropriate card. For unblocking card, your RSA

Token is required. If you still need to speak to a

customer care representative

Click Here for a list of all emergency contact numbers.

-

Select block or unblock a card tab and click the button

on the appropriate card. For unblocking card, your RSA

Token is required. If you still need to speak to a

customer care representative

-

What does it mean to block my card?

- To block a card means that a temporary restriction is place on the card to prevent any further transaction authorization. However, this does not prevent applicable card fees and charges from being generated and monthly payment required.

-

How long after blocking my card can it be unblocked?

- Your card can be unblocked at any time you choose using RSA Token. However, to facilitate further usage, temporary blocked should be removed as soon as possible.

-

If I forget my RSA Token, how can I unblock my card?

-

RSA Token should be reset or you may contact a customer care

representative

Click Here for a list of all emergency contact numbers.

-

RSA Token should be reset or you may contact a customer care

representative

-

Who are cardholders and merchants?

-

-

What is a Dispute?

- A dispute is a complaint filed by a cardholder regarding a transaction posted on his/ her credit card account.

- The dispute is a transaction reversal meant to serve as a form of consumer protection from unauthorised transactions on credit cards, which can be committed by both merchants and individuals.

-

How do I create a dispute on a transaction?

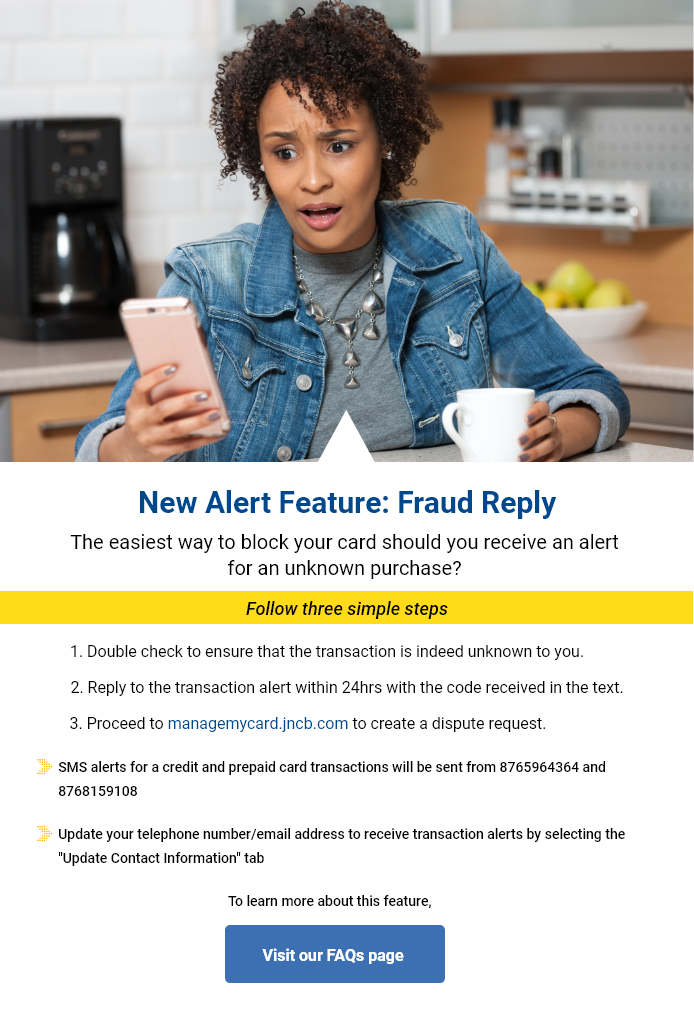

- For unfamiliar transactions (fraud), you may start the process by replying to the transaction text alert which will automatically block your card from any further attempts. Then you proceed to the Create new Dispute tab and follow the steps provided.

- Other types of disputes which are not classified as fraud considering that the transaction would be known to you, kindly proceed to the Create new Dispute tab and follow the steps provided.

-

I did not receive a transaction text message but recognized an unfamiliar transaction done on my card?

- You may immediately proceed to create a dispute using the Create New Dispute tab and follow the steps provided.

-

Do I have to reply using the same keyword in the text?

- Yes, in replying you should type the keyword just as is.

-

Do I have to reply to the text within 24 hours?

- Yes. After 24 hours, the reply feature with the specific keyword will no longer be valid. If you have not responded within 24 hours, kindly proceed to the Create new Dispute tab and follow the steps provided or call Customer Care for assistance.

-

What’s next after replying with the keyword?

- You will receive a second text confirming that your card has been blocked and a replacement card sent to your address. You will then be required to proceed to create the dispute as soon as possible.

-

How do I keep track of the dispute request?

- An email will be sent to you upon receipt of the request and another once the transaction has been processed by the merchant. You can also view the Track your Dispute for updates.

-

Can the dispute request be cancelled?

- Yes, if after 14 days the merchant has not settled, the request can be cancelled, however you may attempt to raise the dispute via the portal once the merchant settles.

-

Can I Update my contact information?

- Yes, you may update your contact information my using the “Update Contact Information” feature to change your cell phone number, email address or mailing address using RSA verification.

-

I replied to the text but the reply failed.

- This could be numerous reasons, you may need to ensure you have credit to send a text, or you may have replied after 24 hours or there could have been a telecom network or system failure at the time. Please immediately, visit the Create new Dispute tab and proceed to raise your dispute or call our Customer Care to assist in creating the dispute.

-

What if I receive a transaction text but no keyword was included in the text?

- If there are no keyword included in your purchase or decline text alert, it could mean that the mobile number we have on records for you is an international number. In this case, you would be required to proceed to Create new Dispute or call Customer Care here for assistance to create the dispute.

-

Will I be able to reply to the transaction alert from an International number?

- No the reply feature will be functional only on local mobile numbers (area code 876, 658). Cardholders with International numbers will be required to visit the managemycard.jncb.com, select Create new Dispute tab and follow the instructions.

-

What is a Dispute?

Step 1 of 3

How satisfied are you with our Customer Dispute Portal?

Step 2 of 3

Is there anything you would like for us to improve? Please share!

Step 3 of 3

Did you find the information and services on the Customer Dispute Portal useful?

Thank you for your feedback.

-

Seeing a suspicious charge on your credit card?

Dispute erroneous, duplicate or

DISPUTE A CHARGE

fraudulent transactions in minutes

-

Seeing a suspicious charge on your credit card?

Dispute erroneous, duplicate or

DISPUTE CHARGE

fraudulent transactions in minutes

CREDIT CARD DISPUTE PROCESS

1

SELECT

"CREATE A DISPUTE"

Login to the Portal using your NCB Online Banking Credentials

2

SELECT

"CREATE A NEW CREDIT CARD DISPUTE"

3

CHOOSE THE CREDIT CARD WITH THE DISPUTED TRANSACTION

4

SELECT DISPUTE OPTION AND FOLLOW THE SIMPLE STEPS PROVIDED

5

SELECT THE TRANSACTION(S) BEING DISPUTED

6

REVIEW AND SUBMIT REQUEST

1

SELECT

"CREATE A DISPUTE"

Login to the Portal using your NCB Online Banking Credentials

2

SELECT

"CREATE A NEW CREDIT CARD DISPUTE"

3

CHOOSE THE CREDIT CARD WITH THE DISPUTED TRANSACTION

4

SELECT DISPUTE OPTION AND FOLLOW THE SIMPLE STEPS PROVIDED

5

SELECT THE TRANSACTION(S) BEING DISPUTED

6

REVIEW AND SUBMIT REQUEST

FIND OUT MORE

UNDERSTANDING DISPUTES

TRACK YOUR DISPUTES

FRAUD PREVENTION TIPS

© Copyright 1999-2018 NCB Jamaica. All Rights Reserved.

Members Of:

![]()

![]()

Members Of:

![]()

![]()